Disclosure rates have nearly tripled in five years. Yet fewer than 2% of companies have actually closed their gender pay gap. For investors and asset managers, the distinction matters.

Pay transparency is now a regulatory reality across much of the developed world. And for financial actors, that creates both an opportunity and an obligation: to look beyond disclosure and interrogate what the data reveals about corporate gender equity.

Equileap’s Gender Equality Report & Ranking 2026, which assessed 3,430 public companies across 24 developed markets, finds that disclosure is accelerating. But closing the gap – actually eliminating the structural pay differential between men and women – remains the exception, not the norm.

Key Finding

Global disclosure of gender pay gap data has risen from 15% in 2021 to 48% in 2026.

Yet only 1.66% of companies have closed their gap — defined as a mean, unadjusted difference of ±3% or less.

Source: Equileap 2026 Gender Equality Report

The Disclosure Revolution: Legislation Drives Accountability

Across every region where disclosure rates have surged, the pattern is unambiguous: mandatory reporting requirements precede meaningful improvement. For investors assessing ESG commitments and regulatory risk, this is a material signal.

Europe has seen the sharpest regional shift. The proportion of European companies publishing gender pay gap data rose from 59% in 2025 to 74% in 2026 — a 15-percentage-point gain in a single year — driven by the EU Pay Transparency Directive, which requires transposition by member states by June 2026. Country-level moves are even more striking: the Netherlands jumped from 38% to 79% disclosure; Germany from 25% to 69%.

Asia-Pacific has undergone a near-complete transformation. In 2022, 91% of companies in the region did not report gender pay data. Today, over 80% do, making it the most transparent region globally. Japan’s Act on Promotion of Women’s Participation and Advancement in the Workforce (2022) and Australia’s tightened disclosure regulations (2023) were the catalysts.

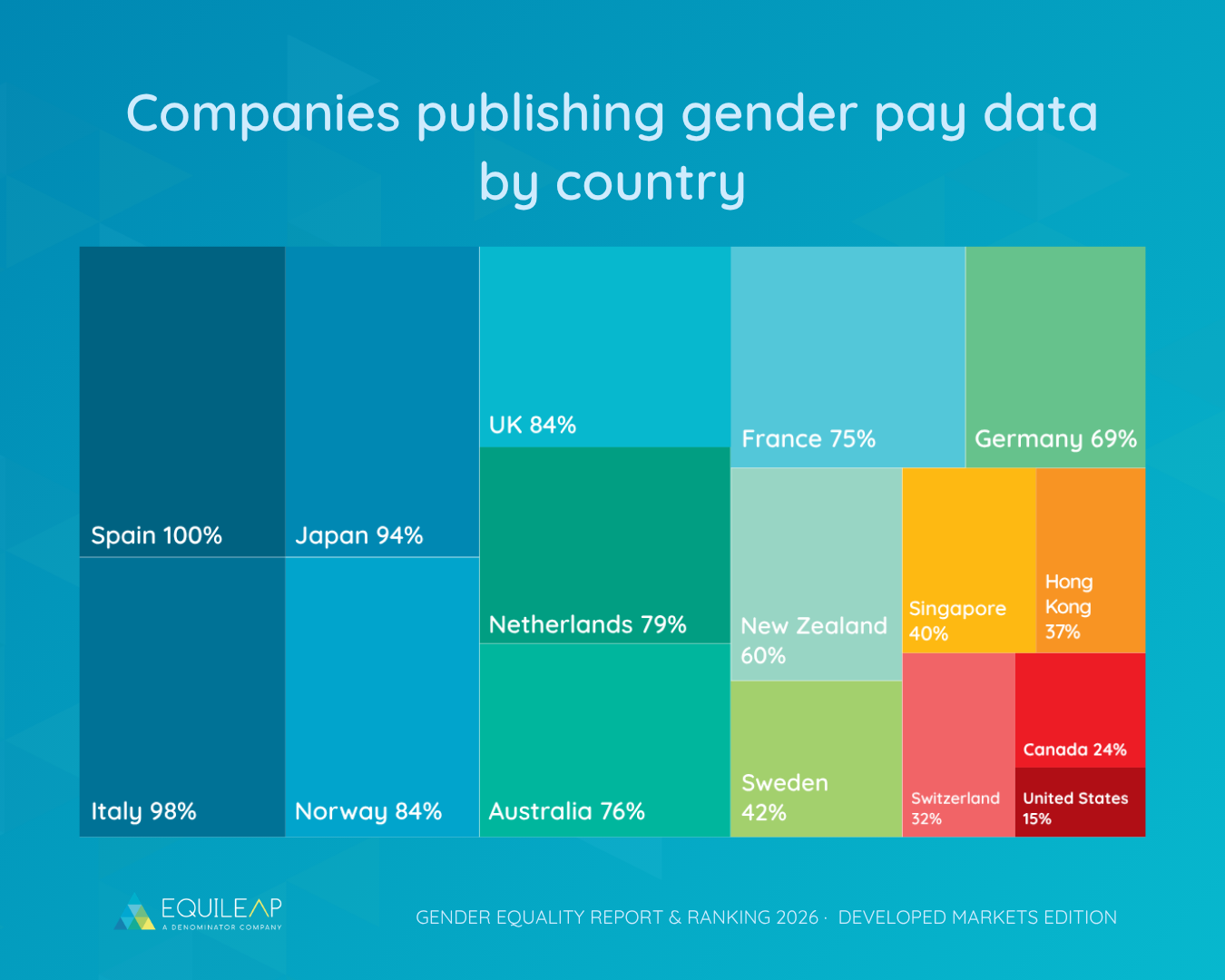

The five highest-disclosure markets globally are all underpinned by legislation:

| # | Market | Disclosure rate | % |

|---|---|---|---|

| 1 | Spain | 100% | |

| 2 | Italy | 98% | |

| 3 | Japan | 94% | |

| 4 | Norway | 84% | |

| 5 | United Kingdom | 84% |

The North America Transparency Deficit: A Governance Risk

Against this global backdrop, North America is an outlier, and a risk factor. Eighty-five percent of North American companies do not disclose gender-disaggregated pay data. The United States has the lowest disclosure rate of any market in Equileap’s analysis: just 15% of US companies publish gender pay gap information, down two percentage points from 2025.

Equileap’s assessment is direct: at the current rate of change, it would take nearly four decades for the US to reach the transparency standards Europe achieved in four years. For investors with exposure to US equities and a fiduciary interest in long-term governance quality and human capital risk, this gap warrants scrutiny.

Who Is Actually Closing the Gap? Six Companies Setting the Standard

Of the small fraction of companies that have both disclosed their pay gap and closed it, six stand out in 2026 for achieving all four of Equileap’s best-practice criteria: publishing an overall gender pay gap, reporting pay gaps across all pay bands, closing the gap within ±3%, and publishing a strategy to maintain that performance.

- Yara International (Norway)

- Enagas (Spain)

- Aena (Spain)

- Dyno Nobel (Australia)

- Italgas (Italy)

- Metcash (Australia)

These companies remain a tiny fraction of the corporate universe. But they represent an investable benchmark, and a replicable model, for what genuine pay equity looks like in practice.

Adjusted vs. Unadjusted: Why the Methodology Matters for Investors

A critical distinction often lost in corporate pay gap reporting (and in ESG scoring) is the difference between adjusted and unadjusted figures. The adjusted pay gap controls for variables such as job title, seniority, and experience, and typically shows a smaller gap. It is sometimes presented by companies as evidence of pay equity.

But the unadjusted gap captures something more fundamental: the structural inequality embedded in an organisation, where women are disproportionately concentrated in lower-paid roles and underrepresented at senior levels.

Equileap’s methodology awards the highest points to companies publishing mean, unadjusted pay gaps precisely because this metric captures systemic inequality rather than like-for-like comparison. Investors and asset managers conducting due diligence or engaging with portfolio companies on gender equity should apply the same standard.

What This Means for Investors and Asset Managers

The 2026 data reinforces three actionable conclusions for financial actors integrating gender pay metrics into investment and stewardship decisions:

- Disclosure is necessary but insufficient. A company publishing a gender pay gap figure is not the same as a company closing one. Stewardship engagement should distinguish between the two and push for meaningful reduction targets.

- Regulatory trajectory is a material factor. The EU Pay Transparency Directive, Australia’s updated rules, and Japan’s reporting requirements have demonstrably shifted corporate behaviour. Investors with exposure to markets ahead of similar reform — particularly the US — should factor in regulatory transition risk and opportunity.

- Demand unadjusted, mean pay gap data. Adjusted figures can obscure structural inequality. Best-practice disclosure — and best-practice investment analysis — should prioritise mean, unadjusted pay gap data across all pay bands.

The trajectory of gender pay gap transparency is encouraging. But disclosure is the beginning of accountability, not the end of it. Companies making real progress — and the investors driving it — are those that have moved from measuring the gap to actively dismantling the structures that create it.

The 2026 data confirms what the past five years have shown: where governments legislate, companies follow. Where they do not, the gap in both disclosure and pay persists.